How to nullify your home loan interest impact ?

Owning a home is one of the top dreams of any individual. In Maslow’s hierarchy of needs, it will probably fit into the base of the pyramid. It is one of the largest investments one will ever make in his/her life. The desire to own a home is very basic, but does everyone have the means to achieve it? Not likely.

That is why, home loans are so prevalent. However, these loans are different from the normal ones. The most striking differences are the long tenure of 20-30 years and large quantum of the loan. This is a secured loan as the property is mortgaged with the bank till it is paid fully.

Due to the loan quantum, your monthly repayment chunk is also very high. It usually forms 30% or higher share of your monthly income.

In this article we will try to minimize your interest impact by exploring easy to implement strategies.

1. Home loan interest impact

The home loan duration in India is usually upwards of 20 years. If we consider 25 years as the median, one can end up paying double the home loan amount taken by the end of the period. Now, this is a lot of wastage. Every penny of the money saved contribute immensely towards the creating a substantial savings safety net. There have been many instances where people take a home loan beyond their means. This leads to severe compromises in their quality of life.

As explained earlier the Home Loan Interest impact is also on the quality of life apart from simple cash outflow. The only reason being the quantum of outflow vis-à-vis the income.

2. Create SIP for HL duration

A very important nugget is to save equivalent of 10% of the home loan EMI into a mutual fund SIP, which will give an annual return upwards of 10%. This small act will help you save on the interest of your home loan if done consistently for the duration of your home loan tenure. Below is an illustrative example.

- Total Home Loan Amount: Rs 57,48,832

- Tenure for EMI: 30 years

- Interest Rate: 7.55 per cent (HDFC)

- EMI per month: Rs 40,394

- Total interest: Rs 87,92,894

- Total Payment: Rs 1,45,41,726

Here, on a loan of Rs 57.48 lakh, you have to repay about Rs 1.45 Cr in 30 years, which is much more than the principal amount. Now we’ll calculate the SIP and its interest amount

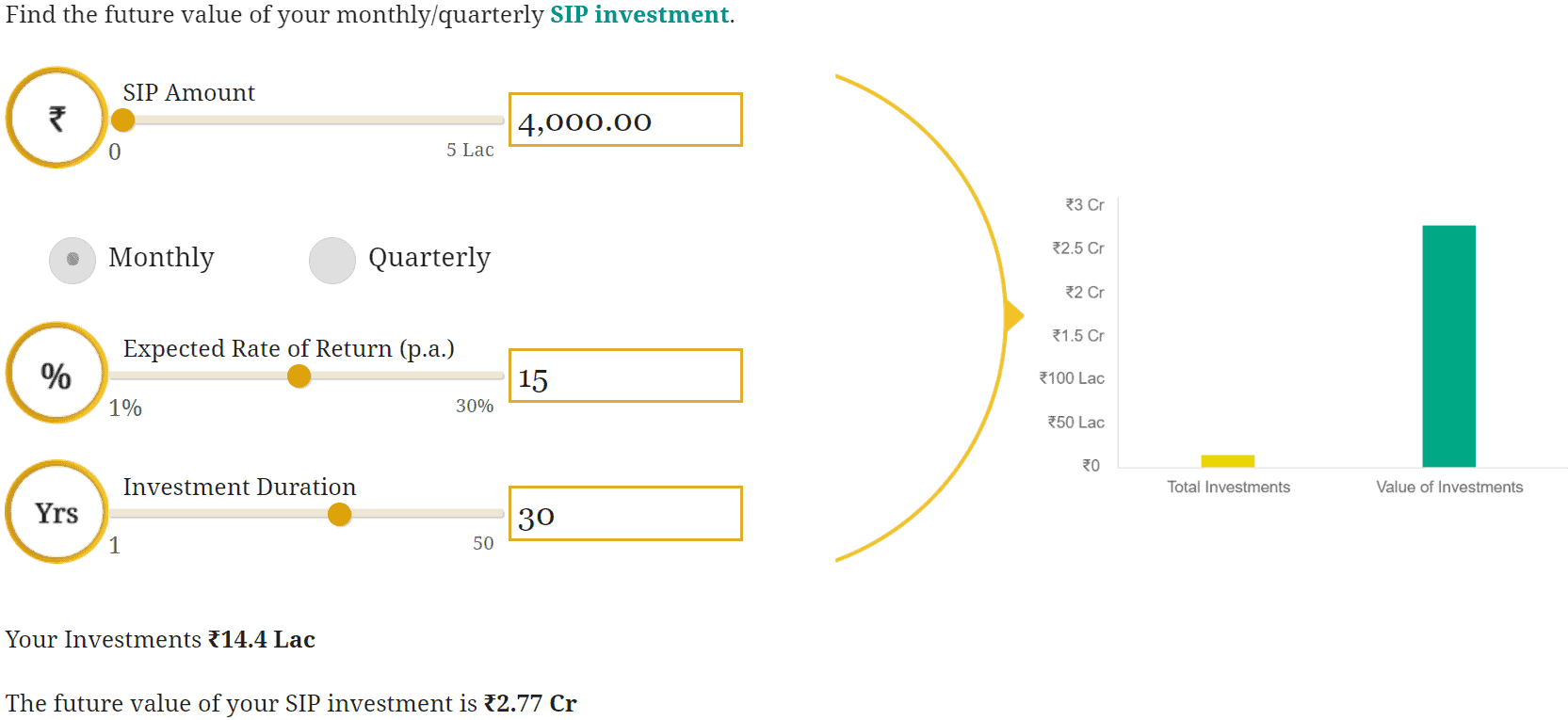

- Monthly SIP: Rs 4,000 (10 per cent of EMI)

- Tenure for SIP: 30 years

- Estimated Return: 15% p.a.

- Amount invested: Rs 14.40 lakh

- Total Value of SIP: Rs 2.77 Cr

Here, you give about Rs 1.45 Cr to the bank in 30 years for a 57.48 lakh loan. At the same time, during these 30 years, by investing only Rs 14.40 lakh in SIP, you can make a corpus of about Rs 2.77 Cr. With this strategy, your interest loss can be reduced to zero along with a surplus.

3. Pay one extra EMI every year

Paying at least one extra EMI will help you save a big chunk of your home loan interest over the tenure of the home loan. As this tenure is usually more than 20 years, even one EMI extra repayment makes a big difference. E.g Rs 40,000 over 20 years, amounts to Rs 8 lakh or more of savings.

It is also important to plan for this extra EMI. Saving every month for the same would make it a cakewalk. Breaking any goal into achievable targets makes the process enjoyable. It is best to budget this every month and plan for it.

4. Add 10% to the EMI every year

As you progress in your career and receive increments every year, try to add at least 10% to the monthly EMI. If done consistently will amount to huge repayments over time. For e.g. if the monthly EMI is Rs 40,000, then you should be able to invest Rs 4,000 via SIP every month. Assuming the loan is of 30 years, you should be able to save more than Rs 14.40 lakh with a maturity amount of Rs 2.77 Cr over that period. This amount would be much more than your interest expense for the Home Loan. Below is an illustration.

5. Reduce loan tenure by making higher down payment

A higher down payment can reduce your tenure tremendously. Thus leading to much higher savings on the interest front. If you have received a lumpsum bonus, consider making a down payment.

You would also be able to save on the Home Loan insurance as a larger down payment has already lowered the principal amount of the loan and hence less coverage is required.

Additionally it will increase your equity. A 10% down payment will lead to only 90% of the property being mortgaged. This would also mean faster repayments and a lower tenure.

6. Wrapping up

The ability to segregate the forest from the trees is an important skill and should be kept in mind when taking a home loan. Many tend to forget or ignore that the interest rate impact, which is roughly equal to the principal amount of the Home Loan or more. EMIs are very effective in numbing the pain. One should be able to use this concept to effectively plan repayments. Strategies like paying an extra EMI every year, saving at least 10% of EMI in a SIP scheme over the period of the loan and making a higher loan down payment will be really effective.

It is now time that you turned the tables in your favor. Go ahead and use the above strategies to nullify the interest rate impact of a home loan. In fact, these strategies can be used for any type of loan that you ever take.

FAQs

Q 1. How many home loans are eligible for tax excemptions?

Ans: There are no restrictions on the number of home loans or houses that are eligible for tax exemptions. However, there are restrictions on the amount eligible for tax relief . For more information, please refer to this article.

Q 2. Can I claim Income Tax exemption on home loan without occupancy certificate?

Ans: This certificate confirms that you are the rightful owner of the property. However, the home loan exemption is based on repayments and can be claimed simply by providing the repayment certificate from the bank.

Q 3. Is home loan covered under 80C?

Ans: Yes, Home Loan principal is covered under Section 80 C of the Income Tax Act. An individual can claim tax deduction under this section on principal repayment with a limit of Rs 1.50 Lakh

Q 4. Is it a good idea to take home loan to save tax?

Ans: The home loan EMI should not be more than 40% of your income. Please keep this ratio in mind and don’t exceed the same to save tax on home loans.

Discover more from Voitto Insights

Subscribe to get the latest posts sent to your email.

Voitto Insights

I am passionate about helping others have the right mindset to overcome challenges. Financial independence plays an important role in having that right mindset. I will also post regarding trading and investment ideas. Earlier had successfully completed two masters in management degrees. I am a working professional with more than a decade experience in multiple industries. Disclaimer: Kindly note that, I am not a Sebi registered investment advisor. Please do your own due diligence before taking any action on the posts here. All posts are for educational purposes only.

You May Also Like

Insightful lessons from the life of Mr. Rakesh Jhunjhunwala !

Outsource Your Repetitive Tasks to AI !