How to manage family money for a better future?

- 1. Introduction

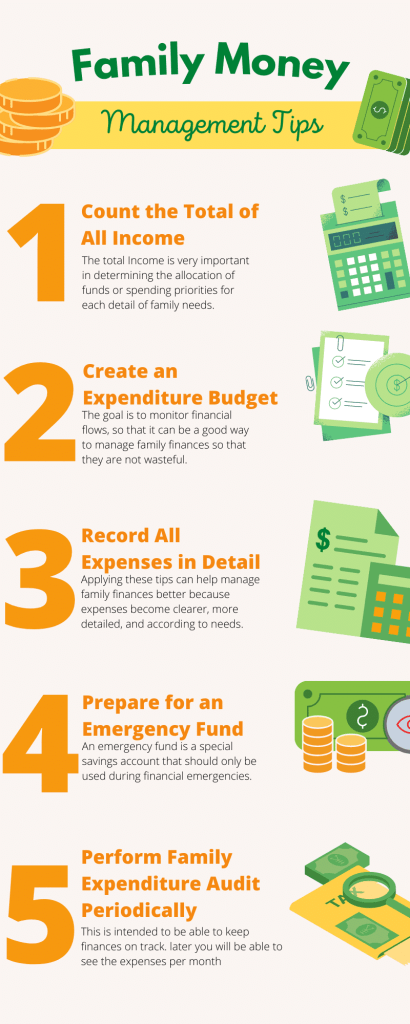

- 2. Total family income count

- 4. Creating realistic budget that works

- 3. Learn to spend wisely

- 4. Establish a budget for entertainment costs.

- 5. Record detailed expenses

- 6. Creating emergency fund

- 7. Periodic family expense track and audit

- 8. Investing Tips for Families to Grow their Wealth and Secure their Future

- 9. Final thoughts

1. Introduction

Family financial management is an important part of managing one’s household budget and planning for the future. It involves setting goals, tracking expenses, making decisions about how to use income, and investing wisely.

By taking the time to understand family financial management, individuals can make sure that their money is working for them in the most effective way possible.

With proper family financial management, individuals can ensure that they are able to provide for their families and plan for a secure future.

2. Total family income count

Recording family income count is an important task for any family. It is essential to keep accurate records of both monthly and yearly income in order to make informed decisions about budgeting, saving, and investing.

To accurately record family income count, it is important to factor in income cuts such as taxes, health insurance premiums, and other deductions.

Additionally, it is important to track any rental or business income as well as salary or pension income.

Scholarships should also be taken into account when tracking family income count so that the full picture of the family’s financial situation can be seen.

The following methods are some of the ways to accurately record family income:

• Average Weekly Earnings: This is an average of all the earnings a person receives during one week.

• Income in April 2016: This is total income that was received by someone during April 2016, with no specific changes or deductions.

• Total Family Income for the Year: A person’s total monthly income plus any amount they receive like Social Security or disability benefits. .

• Total Monthly Income: This is the total amount of money someone received in one month, before any deductions or changes are made. .

• Regardless of other income, this is the total monthly income for someone who does not have any specific changes or deductions made.

4. Creating realistic budget that works

Creating a family budget can be an intimidating task, but it doesn’t have to be. With the right tools and strategies, you can create a practical and realistic budget that works for your family’s needs.

By understanding your income and expenses, setting goals, tracking spending, and making adjustments as needed, you can create a budget that will help you achieve financial stability.

With a well-crafted budget in place, you’ll be able to save more money and reduce stress related to money management. Know how much you can spend without going into debt and stick to it.

3. Learn to spend wisely

There are many small things you can do to cut back or avoid spending on unnecessary items that add up quickly. These could include avoiding fast food or buying past-its-prime meat, where you live or not stopping at the grocery store when you’re running low on groceries.

When it comes to shopping, do some price comparisons before heading out the door and only buy what is needed, nothing more.

4. Establish a budget for entertainment costs.

Spending money on entertainment is something that everyone does from time to time and it’s not always easy knowing where

5. Record detailed expenses

Knowing where your money is going and how much you are spending is one of the most important steps in managing your finances. Recording detailed family expenses can help you stay on top of your finances and make sure that you are not overspending.

By taking a look at your check account statements and categorizing expenses into needs, wants, debt payments, and savings, you can easily record all of your family’s expenses.

Needs = Rent, utilities, groceries, toilet paper.

Wants = Vacation, travel expenses.

Debt payments = Mortgage or other loans with due dates.

Savings = Savings account and rainy day fund (not recommended to be used until your emergency fund is established).

This will allow you to keep track of where exactly your money is going and make sure that it is being used wisely. With this information, you can better plan for the future by setting financial goals such as saving for retirement or paying off debt. .

6. Creating emergency fund

An emergency fund is an important financial tool to have. It can help you cover unexpected expenses and provide financial security in times of need. Creating an emergency fund involves different strategies such as setting aside 12 months worth of your living expenses, investing in mutual funds, and putting money into fixed deposits.

Having an emergency fund gives you the liquidity to handle any unforeseen circumstances without having to dip into your savings or take out a loan. It is important to have a plan for creating an emergency fund that works best for you and your family’s needs.

This emergency fund should be accessible to you and your family in the event of a job loss, medical bill and/or natural disaster. The money should be saved in a separate bank account that is not connected to your checking account (unless you have no other options).

You should avoid using credit cards for this emergency fund, as this will make it easier to borrow against the money. Borrowing on a credit card can quickly lead to overspending and high interest rates. Plus, the interest may not be tax deductible if you are in higher tax brackets.

7. Periodic family expense track and audit

Tracking and monitoring your personal finances is one of the most important steps you can take to ensure that you stay within your budget and reach your financial goals.

With the right tools, you can easily track your income, expenses, debts, investments, and more. This will help you stay on top of your finances and make sure that you are making smart decisions with your money.

In this article, we’ll discuss some tips on how to track and monitor your personal finances so that you can stay within the plan. you put together.

#1: Track your spending patterns First and foremost, track how you’re spending your money. Many people have a difficult time coming up with a plan to get out of debt or make more money because they don’t know where their money is going. It’s important to keep track of your expenses so that you can adjust them accordingly. We recommend using an app like Mint that helps users see their transactions in one place and keep track of when they’ve spent the most, but it’s up to you what apps you use for this purpose!

8. Investing Tips for Families to Grow their Wealth and Secure their Future

Investing is a great way for families to grow their wealth and secure their future. Whether you’re a beginner or an experienced investor, there are certain tips that can help you make the most of your investments and ensure that your family’s financial security is taken care of.

For those new to investing, the tips below are a great way to get started. For the experienced investor, check out this article for some new insights.1. Investing is about taking advantage of opportunities.

Investing is all about benefits and making money. You don’t need a lot of capital to make smart investments in order to grow your wealth and secure your future.

If you want to invest, start with this basic principle: “What can I learn from what others have done?” The more you know about investing strategies that other people use successfully, the more easily you can build your portfolio.

9. Final thoughts

Managing family money can be a daunting task, but with the right strategies in place, it can be done efficiently and effectively. By understanding the needs of the family and setting realistic goals, you can ensure that everyone’s financial needs are met.

Additionally, budgeting is an important tool to help manage family money and ensure that long-term financial goals are met. Finally, communication is key when it comes to managing family money as it helps to keep everyone on the same page.

With careful planning and regular communication, managing family money does not have to be a difficult task.

You can tackle this subject by asking the following questions:

What are your values?

What is important to you about money?

How do you feel about being in debt?

Do you know your net worth?

Do you have a budget or spending plan for the month that includes all income and expenses, as well as planned savings for emergencies and major purchases?

Discover more from Voitto Insights

Subscribe to get the latest posts sent to your email.

Voitto Insights

I am passionate about helping others have the right mindset to overcome challenges. Financial independence plays an important role in having that right mindset. I will also post regarding trading and investment ideas. Earlier had successfully completed two masters in management degrees. I am a working professional with more than a decade experience in multiple industries. Disclaimer: Kindly note that, I am not a Sebi registered investment advisor. Please do your own due diligence before taking any action on the posts here. All posts are for educational purposes only.

You May Also Like

The Mind-Blowing Truth why 99% of People set Goals Wrong!

How do credit cards levy different charges? An in-depth look.