How do credit cards levy different charges? An in-depth look.

1. Introduction

Have you ever struggled to understand the various Credit Card charges levied?

Credit Cards are a convenient tool for managing your finances. They make purchases easier. However, they can also prove to be heavy on your pocket.

Credit cards also come with fees and charges, such as interest rates and late payment fees. Understanding how credit cards calculate these charges is important for managing your finances effectively.

They offer a variety of benefits, including rewards programs and the ability to build a sound credit history.

In this article, we will take a closer look at how credit cards calculate interest and other charges, including late fees and balance transfer fees.

2. Interest rates and how they’re calculated

The interest rate on a credit card is the cost of borrowing money from the issuer. It’s expressed as an annual percentage rate (APR), and it’s important to note that interest rates can vary widely from card to card.

The interest rate on your credit card can significantly impact your overall balance. It’s important to understand how it’s calculated.

i. How are Interest rates calculated using the average daily balance method ?

The average daily balance approach is commonly used to determine interest charges on credit cards.

Your credit card’s average daily balance is computed by adding the balances from each day’s end in the billing cycle.

The interest you pay on your credit card will be calculated from this daily average.

To illustrate, imagine you had a $1,000 balance on a credit card with an APR of 18%. It will cost you $180 in interest to keep this balance open for a year.

But if you pay your payment in whole and on time each month, you won’t have to worry about interest.

The balance you carry forward, along with any subsequent purchases you make with your credit card, will accrue interest until the balance is paid in full.

ii. Importance of billing cycle

Your monthly credit card statement will include two important dates: the statement date and the payment due date.

The statement date is the day your bank will generate a statement for the expenses incurred during the previous month or billing cycle.

The date on which the balance listed on the invoice must be paid in full is known as the due date.

Customers are often given a grace period of 20-25 days from the statement date. They must use this time to pay any amounts that are still overdue.

Let’s say the first of April is the date of your credit card statement. Your March 1 account will include charges for the billing cycle, with payment due date between April 20 and April 25.

You can enjoy almost 50-55 days of interest-free/grace credit if you made a transaction on March 2. If you make a purchase on March 29th, however, you will only have 21–26 days to use your grace period.

You can make the most of your 20-25 day interest-free/grace period by timing your purchases to coincide with your billing cycles.

You won’t have to pay any interest as long as you pay off your balance in full each month. Only if unpaid sums from the previous month are carried over into the current month will interest be due.

Banks are allowed to provide variable interest rates based on customer risk profile. A monthly rate of 3% is among the highest possible. But, the APR could change depending on your credit history and how often you use the card.

3. Late Payment Fees and How They’re Calculated

i. What are late payment fees?

Late payment fees are typically a flat fee, meaning that the amount you’re charged does not depend on the balance on your credit card. For example, if your minimum payment is $25 and you miss the due date, you may be charged a $40 late payment fee.

ii. How are late payment fees calculated?

Late payment fees are another common charge that credit card issuers may assess.

You must make your minimum payment by the due date. If you don’t, you will likely be charged a late payment fee.

Late payment fees can range from $25 to $40 or more, and they can add up quickly if you’re not careful.

4. Balance transfer fees and how are they calculated

Balance transfer fees is another type of charge that you may encounter with a credit card. Balance transfers allows you to transfer the balance from one credit card to another, typically with a lower interest rate.

However, credit card issuers may charge a fee for this service, which is typically a percentage of the balance being transferred.

Fees for transferring a balance can be as high as 5% of the amount transferred. So keep that in mind if you’re thinking about doing so. If the balance transfer fee on your new credit card is 3%, for instance, you’ll have to pay $150.

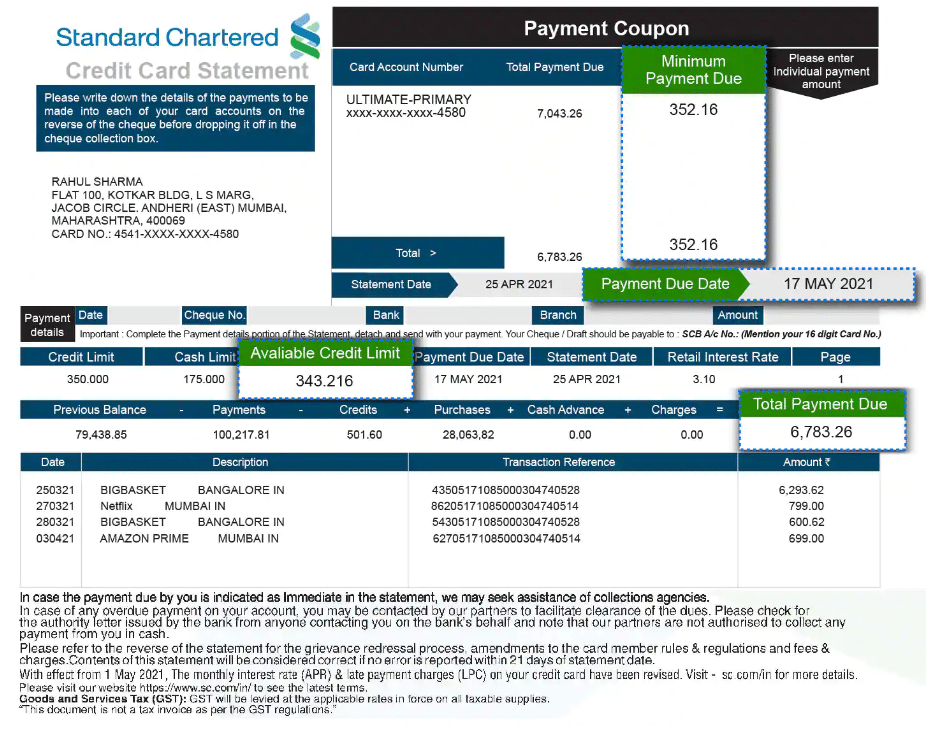

5. Understanding Credit card statements

When you use your credit card to make purchases or payments, the details of these transactions are recorded by your credit card issuer and are summarized in your credit card statement.

i. Breakdown of charges

Here’s a breakdown of how charges are listed on a credit card statement:

Transaction date: This is the date when the transaction occurred, i.e. when you made the purchase or payment.

Merchant name: This is the name of the business where the transaction took place. It could be a physical store or an online retailer.

Transaction amount: This is the dollar amount of the transaction, including any taxes or fees associated with the purchase.

Transaction type: This identifies whether the transaction was a purchase, a cash advance, a balance transfer, or a fee.

Payment received: This section shows the payments you’ve made towards your credit card balance.

Interest charges: If you have an outstanding balance on your credit card, you may be charged interest on that balance. This section will list the interest charges applied during the billing period.

Fees: This section will list any fees associated with your credit card, such as annual fees, late payment fees, or balance transfer fees.

Rewards earned: If you have a rewards credit card, this section will list the rewards you’ve earned during the billing period.

Balance: This is the total amount you owe on your credit card, including any outstanding balance from previous billing cycles, new purchases, fees, and interest charges.

By reviewing your credit card statement regularly, you can keep track of your spending, identify any errors or fraudulent charges, and manage your credit card balance effectively.

ii. Tips for reading and understanding a credit card statement

Reading and understanding a credit card statement is an important part of managing your credit card account effectively. Here are some tips to help you read and understand your credit card statement:

Review your statement regularly: It’s important to review your credit card statement regularly, usually monthly, to ensure that you’re aware of all the transactions made on your card, as well as any fees, interest charges, or rewards earned.

Check for errors: Make sure to double-check all the transactions listed on your statement to ensure they are accurate. If you notice any errors or fraudulent charges, contact your credit card issuer immediately to dispute the charges.

Understand your payment due date: Your statement will list the payment due date, which is the cut off date by which you need to make your payment. Make sure to pay your balance in full by this date to avoid late payment fees and interest charges.

Know your credit limit: Your statement will also list your credit limit, which is the maximum amount you can spend on your credit card. Make sure you don’t exceed this limit, as you may be charged over-limit fees and it can negatively impact your credit score.

Understand interest charges: If you have an outstanding balance on your credit card, you may be charged interest on that balance. Make sure to review the interest rate listed on your statement and understand how interest is calculated. You should try calculating yourself.

Pay attention to fees: Your statement will list any fees associated with your credit card, such as annual fees, late payment fees, or balance transfer fees. Make sure to understand these fees and try to avoid them whenever possible.

Understand rewards programs: If you have a rewards credit card, make sure to review the rewards section of your statement to understand how rewards are earned and redeemed.

By following these tips, you can better understand your credit card statement and manage your credit card account effectively.

iii. Importance of monitoring charges on a credit card statement

Monitoring charges on your credit card statement is extremely important to ensure that you’re aware of all the transactions made on your card, and to detect any errors or fraudulent charges that may have been made. Here are some reasons why it’s important to monitor your credit card statement regularly:

Detect and prevent fraud: By reviewing your credit card statement regularly, you can quickly detect any unauthorized charges or suspicious activity on your account. This allows you to take action immediately and prevent further fraudulent charges from being made.

Ensure accuracy: Credit card statements can sometimes contain errors, such as double charges or incorrect amounts. By monitoring your statement regularly, you can catch these errors early and report them to your credit card issuer to have them corrected.

Avoid late payments: Your credit card statement will list the payment due date, and if you miss this date, you may be charged a late payment fee and your credit score could be negatively affected.

By monitoring your statement regularly, you can ensure that you make your payments on time.

Manage your budget: By reviewing your credit card statement, you can track your spending and identify areas where you may need to cut back. This can help you manage your budget effectively and avoid overspending.

Maximize rewards: If you have a rewards credit card, monitoring your statement can help you ensure that you’re earning rewards for all eligible purchases. This can help you maximize the rewards you earn and take full advantage of your credit card benefits.

6. Tips for avoiding Credit card charges

Avoiding credit card charges is important for maintaining good financial health. Here are some tips for avoiding credit card charges:

Pay your balance in full each month: Paying your credit card balance in full each month can help you avoid interest charges, late fees, and other charges that can add up quickly.

Avoid cash advances: Cash advances come with high-interest rates and fees, making them an expensive way to borrow money. Avoid using your credit card for cash advances whenever possible.

Monitor your credit card statement: Review your credit card statement regularly to ensure that there are no unauthorized charges or errors. If you spot any discrepancies, report them to your credit card issuer immediately.

Use your credit card responsibly: Use your credit card only for purchases that you can afford to pay off in full each month. Avoid overspending or using your credit card to make purchases that you can’t afford.

Avoid balance transfers: Balance transfers can be a useful tool for consolidating high-interest debt, but they often come with fees and introductory interest rates that can increase over time. Avoid using balance transfers unless you have a solid plan for paying off your debt quickly.

Opt-out of over-limit fees: If you don’t want to risk going over your credit limit and being charged an over-limit fee, consider opting out of this service with your credit card issuer.

Negotiate with your credit card issuer: If you’re struggling to make payments, contact your credit card issuer and ask if they can waive late fees or reduce your interest rate.

7. Importance of managing Credit card charges

i. Impact of credit card charges on overall financial health

Credit card charges can have a significant impact on overall financial health. Here are some ways credit card charges can affect your finances:

High-interest charges: Credit card balances typically come with high-interest rates, which can accumulate quickly if you don’t pay off your balance in full each month.

This can result in paying hundreds or even thousands of dollars in interest charges over time, which can negatively impact your overall financial health.

Debt accumulation: If you’re not careful, credit card charges can accumulate quickly and lead to debt. High levels of debt can cause stress and anxiety, and may impact your ability to achieve other financial goals such as saving for retirement or buying a home.

Late fees: If you miss your credit card payment due date, you may be charged a late fee. These fees can add up quickly and impact your overall financial health.

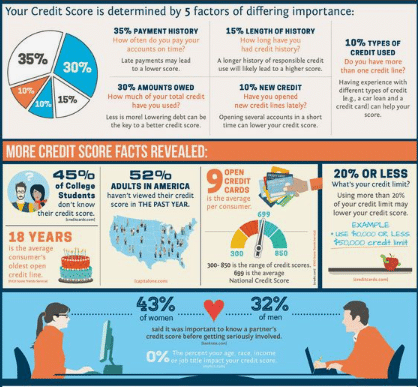

Credit score impact: Credit card charges can impact your credit score, which can affect your ability to get approved for loans or credit in the future. Late payments, high credit utilization, and a history of missed payments can all negatively impact your credit score.

Opportunity cost: When you use your credit card for purchases, you may be missing out on the opportunity to earn interest or invest your money elsewhere. This can impact your overall financial health by reducing the potential returns on your investments.

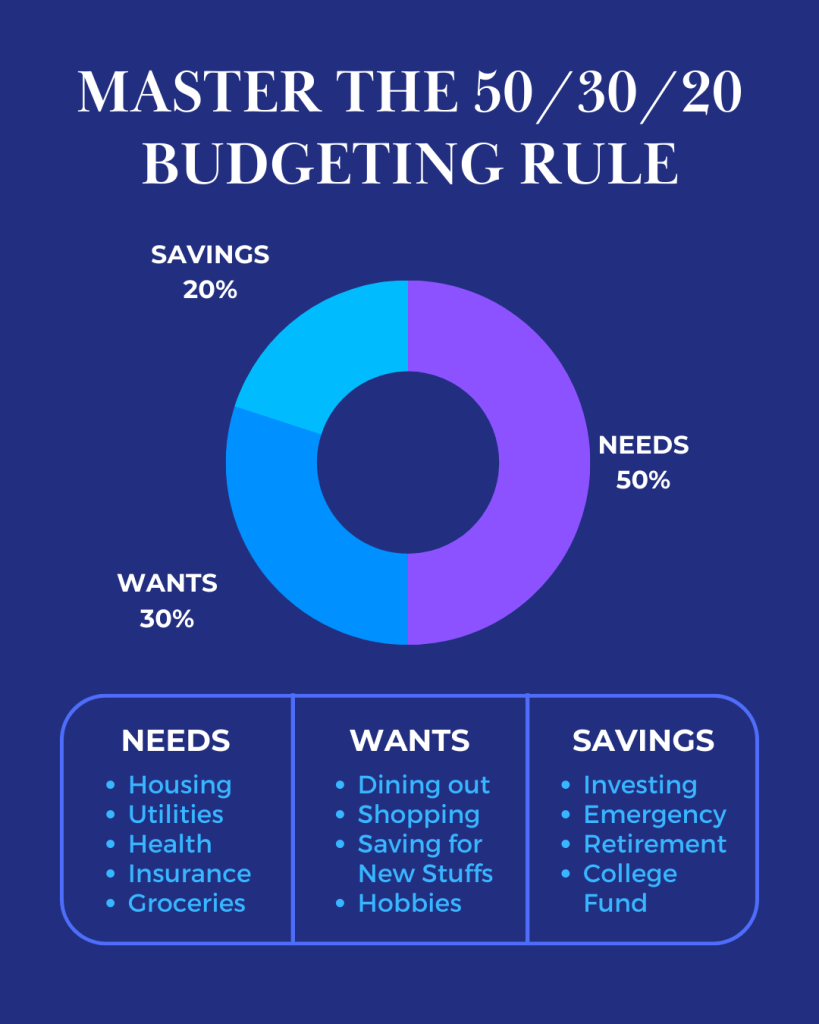

ii. Importance of budgeting and managing credit card charges

Budgeting and managing credit card charges are crucial for maintaining good financial health. Here are some reasons why budgeting and managing credit card charges are important:

Avoiding debt: Budgeting helps you plan your spending and avoid overspending, which can lead to credit card debt. By managing credit card charges within your budget, you can ensure that you’re not spending more than you can afford to pay off in full each month.

Maintaining good credit: Managing credit card charges responsibly can help you maintain a good credit score. A good credit score is important for getting approved for loans, credit cards, and other financial products, and can help you get better interest rates and terms.

Minimizing interest charges: By managing credit card charges effectively, you can avoid high-interest charges that can accumulate quickly and make it harder to pay off your balance. This can save you hundreds or even thousands of dollars in interest charges over time.

Maximizing rewards: By budgeting and managing your credit card charges, you can take advantage of rewards programs and earn cashback, points, or other rewards for your purchases. This can help you save money and get more value out of your credit card.

Achieving financial goals: By budgeting and managing credit card charges, you can free up money to put towards other financial goals, such as saving for retirement, buying a home, or paying off other debts.

8. Final thoughts

In conclusion, credit card charges can have a significant impact on overall financial health. It’s important to use credit cards responsibly, pay off balances in full each month, and monitor your credit card charges regularly to avoid debt, late fees, and other negative consequences.

You as a Credit Card holder should know the billing cycle and charges that come with it.

Budgeting and managing credit card charges are essential for maintaining good financial health. By staying within your budget, avoiding debt, and maximizing rewards, you can manage your credit card charges effectively and achieve your financial goals.

It is best to compare between multiple card features before committing to anyone. You should try to find a rewards based card, which syncs with your spending habits and provides the maximum benefits.

FAQs

1. Do credit card companies ever make mistakes on card balance?

Ans. It is rare that a Credit Card provider will make a mistake in calculating your interest or outstanding monthly balance. However, mistakes are very much possible and you should go through your credit card statement carefully.

Once you have identified a mistake, you should quickly connect with the service provider on email as well as call center to ensure fast resolution. This is also called disputing the transaction.

2. Is it better to make several credit card payments during a period?

Ans. The interest accrues on average daily balance. As a result, if you make several payments during a billing cycle, the interest charge reduces.

If this article shifted your perspective , Please buy me a coffee, subscribe, share, comment, or like/clap.

Check out the free library here –Free Library – Voitto Insights

Click for exciting curated offers – linktr.ee/voittoinsights

For more insightful articles visit – voittoinsights.in

Nothing satisfies me more than helping you achieve your true potential.

Discover more from Voitto Insights

Subscribe to get the latest posts sent to your email.

Voitto Insights

I am passionate about helping others have the right mindset to overcome challenges. Financial independence plays an important role in having that right mindset. I will also post regarding trading and investment ideas. Earlier had successfully completed two masters in management degrees. I am a working professional with more than a decade experience in multiple industries. Disclaimer: Kindly note that, I am not a Sebi registered investment advisor. Please do your own due diligence before taking any action on the posts here. All posts are for educational purposes only.

2 Comments

Pingback:

Pingback: